Features

Industry News

Markets

2022 lumber markets outlook

Paul Jannke, principal of Forest Economic Advisors LLC, provides a forecast of international and domestic lumber markets in the coming year.

January 10, 2022 By Paul Jannke

Photo: Annex Business Media.

Photo: Annex Business Media. It’s been a wild ride for wood products, particularly lumber, over the past two years. From a recession in the second quarter of 2020 to record high prices just one year later, participants in these markets are left with many questions, especially where prices are headed. To answer these, one must start by looking at the drivers for lumber demand, with U.S. housing being the primary.

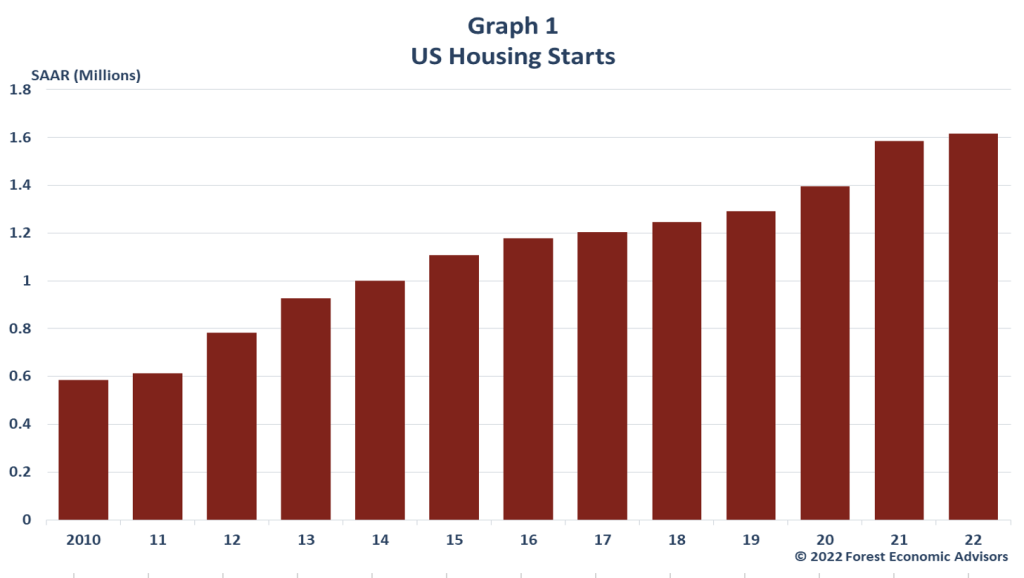

With the U.S. economy and employment growing robustly in 2021 and 2022, interest rates remaining low by historical standards, many of the supply-side constraints that held back housing over the past half-decade resolved, and high pent-up demand, we expect housing starts will continue to grow from an average of 1.584 million units in 2021 to 1.618 million in 2022. Strong pent-up and demographic demand would push housing starts significantly higher (likely to average 1.80-2.00 million units) were it not for some continued supply-side constraints, with labour and materials being the main ones.

Rising home equity and a lack of new-entry and first-move-up homes will cause homeowners to fix up rather than move up. In addition, the housing stock is aging. The average home is now over 40 years old, and home sizes at that time averaged 1,750 square feet, which is significantly below today’s level. This means individuals are likely to add on when they purchase these older homes, keeping residential expenditures from dropping too dramatically. Residential-improvement expenditures increased 0.5 per cent in 2021 and will fall 5.4 per cent in 2022.

After declining in much of 2019, U.S. industrial and furniture production both rebounded throughout 2020 and 2021. Industrial production saw steady growth, as manufacturing increased every quarter, while furniture production experienced a rockier recovery. We expect growth for both to continue through the end of the forecast, with industrial-production index anticipated to increase 3.6 per cent and furniture production 2.5 per cent in 2022.

Over the past six quarters, nonresidential-construction expenditures have fallen. However, we expect the declines to have ended in the fourth quarter of 2021, with nonresidential-construction expenditures then increasing each quarter of this year. We expect nonresidential-construction expenditures fell to $636.00 billion in 2021 before they recover to $649.40 billion this year.

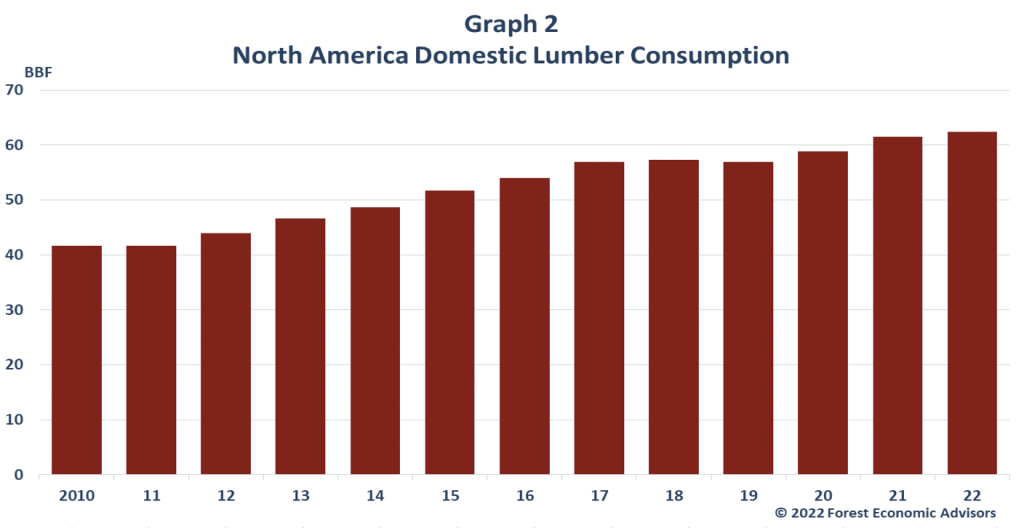

With most end-use markets continuing to show strength, we estimate North American lumber demand was up 3.6 per cent for 2021. However, we expect North American lumber demand to grow just 1.4 per cent in 2022. Based on this, we expect North American demand reached 64.78 BBF last year and will hit 65.67 BBF this year.

North American softwood lumber demand is primarily driven by U.S. consumption. U.S. softwood lumber consumption rose to 50.93 BBF in 2020, and we are estimating an increase to 52.76 BBF in 2021, the highest level since 2006; and forecasting 53.87 BBF in 2022. Growth in Canadian lumber consumption was primarily driven by residential-improvement markets, which will benefit from years of strong home sales. However, Canada’s manufacturing sector will then be weakened as the Canadian dollar strengthens, so we expect consumption to fall year over year from the fourth quarter of 2021 through the second quarter of 2022 before picking back up over the remainder of the forecast period.

Between the second quarter of 2019 and the second quarter of 2021, North American offshore exports averaged a decline of nearly 24 per cent year over year. As things improved worldwide last year, we are estimating that offshore lumber exports from North America fell slightly less in 2021, likely 9.8 per cent from 2020 (compared with a 25.7 per cent decline the previous year). We expect export growth will remain weak, falling another 1.6 per cent in 2022 because of strong domestic consumption, high prices, and competition from Europe.

Lumber supply is made up of domestic capacity plus imports. Lumber demand and prices plunged early in 2020Q2. That, combined with uncertainty around the COVID-19-induced recession, caused mills to slash capex. Consequently, capacity declined slightly in 2020. Contrary to expectations, prices surged, and mills began investing to take advantage of the higher prices. This will push capacity one per cent higher in 2021-22. Significant new capacity and expansions at existing facilities have been announced over the next two years. Constraints on machinery manufacturers and labour at the mills will cause a slow ramp-up for this capacity.

U.S. offshore imports jumped nearly 40 per cent in 2020 and, with demand and prices surging in early 2021, offshore imports are expected to have increased an additional 13 per cent for 2021. We expect further growth of 9 per cent in 2022.

There are several reasons for our forecast strength in imports, including strong North American consumption and elevated prices; capacity limitations in Canada; abundant, cheap fibre supply in central Europe; and the strong U.S. dollar. See FEA’s study Central European Beetle and Windstorm Timber Disaster for a detailed explanation of the fibre-supply situation in central Europe.

Demand on U.S. mills (consumption plus exports minus imports) has come off its seasonal peak, and we expect demand on U.S. mills will remain weak through February due to a combination of slipping residential-improvement markets and the normal seasonal decline in end-use market activity. Putting it all together, we expect that, after holding flat last year, total demand on North American mills rebounded by 3.3 per cent last year and will grow another 1.1 per cent this year.

Capex ground to a halt in the first half of 2020. This slowed capacity growth into 2021. Meanwhile, demand was strong and grew robustly in the first half of 2021. This pushed operating rates up to 87 per cent for the year. Demand will continue to grow in 2022, but capacity expansions following the 2020−21 surge in prices will begin to come online. This will cause the demand/capacity ratio to remain flat at 87 per cent in 2022.

Putting that all together, we can now turn to lumber prices. Prices ended the year with a rally. Part of this was because of acute supply disruptions due to the extremely wet weather in British Columbia. But a portion of the rising prices was driven by strong demand as warm weather across the country has extended the building season while dealers, afraid of another run-up in prices similar to the spring of 2021, sought to replenish inventories. The effects of the weather will be short-lived. However, we expect prices will continue to remain elevated through February, for several reasons.

Inventories across the supply chain remain low, and dealers will want to start building them back before the construction season across much of North America begins in March-April. Mills also took downtime around the holidays. Finally, all-too-fresh memories of $1,000-plus prices will keep buyers in the market while log- and labour-supply constraints hamper production.

Lumber prices in early 2022 will be bolstered by supply constraints in the U.S. South. Capacity expansions in the U.S. South have mostly made up for British Columbia mill closures. However, wet weather and labour-supply constraints have limited log availability and mill production. We expect soil moisture content will decrease over the winter, with 2021-22 expected to be a La Niña year. This will ease the difficulty of getting into the woods. Labour constraints will be a bit more long-lived, as many folks who left the workforce at the beginning of the COVID-19 pandemic have yet to return, and we expect labour issues will continue to hamper production this year.

While we expect prices will remain elevated into early 2022, we do not expect them to get anywhere near their 2021 levels. Capacity additions in the U.S. South, relatively higher inventory levels coming into the year, and weaker residential-improvement activity will all prevent a run similar to what we saw in 2021. Moreover, we expect prices will slip in the second quarter as dealers digest the inventories they built in late 2021 and early 2022. We do expect another round of buying in the third quarter as residential-construction markets remain strong seasonally and cyclically; however, prices in the second half of 2022 will average below the first half of the year as even more low-cost southern pine capacity comes online. For the year, we expect the RLFLCI will average 645 in 2022.

Ultimately, we expect lumber prices will continue to be volatile in 2022. There are a number of reasons for this, but the main one is the lingering effects of COVID-19. The lack of buying and production in the wake of COVID-19 first breaking out in the U.S. drove dealer stocks to historic lows. As demand surged, there was not enough inventory in the system to supply the increased consumption. This caused prices to soar to record levels. At those high prices, dealers stopped buying lumber, again driving down their stocks. Low stocks will likely force dealers to buy wood at higher prices than they want, and those high prices will cause dealers to stop buying as soon as they meet their immediate needs, which in turn will force prices sharply lower. This cycle will repeat itself over the next year, causing prices to be extremely volatile.

Paul Jannke is a principal of Forest Economic Advisors (FEA) LLC, the premier source for North American wood products analysis and information. Paul’s main area of expertise is North American lumber markets. Having spent nearly 30 years analyzing lumber markets and providing reliable, insightful forecasts, Paul is the industry’s top economic analyst. He is the author of FEA’s Lumber Advisor and Lumber Quarterly Forecasting Service publications.

Paul Jannke is a principal of Forest Economic Advisors (FEA) LLC, the premier source for North American wood products analysis and information. Paul’s main area of expertise is North American lumber markets. Having spent nearly 30 years analyzing lumber markets and providing reliable, insightful forecasts, Paul is the industry’s top economic analyst. He is the author of FEA’s Lumber Advisor and Lumber Quarterly Forecasting Service publications.

Print this page