Features

Markets

2023 Lumber markets outlook: Short-lived growing pains in the forecast

January 24, 2023 By Paul Jannke

Photo: Annex Business Media

Photo: Annex Business Media Rising interest and mortgage rates will most likely cause economic activity to slow in 2023, painting a pessimistic picture for North American housing and, consequently, lumber markets over the next year, forecasts U.S.-based Forest Economic Advisors, LLC (FEA).

This is expected to be short lived, however, with optimism on the horizon the following year when FEA, the premier source for North American wood products analysis and information, expects to see an uptick in the economy.

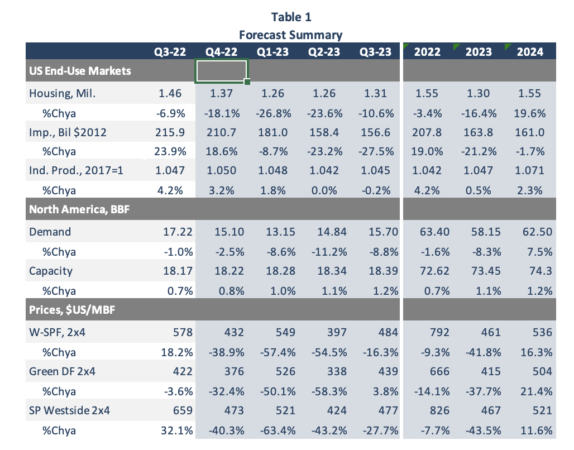

Home building, along with mortgage rates and purchasing power, have a direct impact on lumber demand as the majority of North American houses are constructed with wood. A flurry of recent rate hikes leads FEA to forecast that U.S. housing starts will drop 16 per cent year-over-year in 2023 to 1.3 million before rebounding to 1.55 million in 2024 as the general economy is expected to pick up (Table 1).

Source: Forest Economic Advisors

The strong fundamentals – record pent-up demand, the large population of adults in prime home-buying years, record home equity, the aging housing stock, and historically low inventories of homes for sale – that contributed to the surge in demand during the pandemic (when rock-bottom interest rates sent homebuyers into a buying frenzy and caused prices to soar) are still simmering below. With these factors underpinning softwood lumber’s main end-use market, housing starts will remain above pre-pandemic levels.

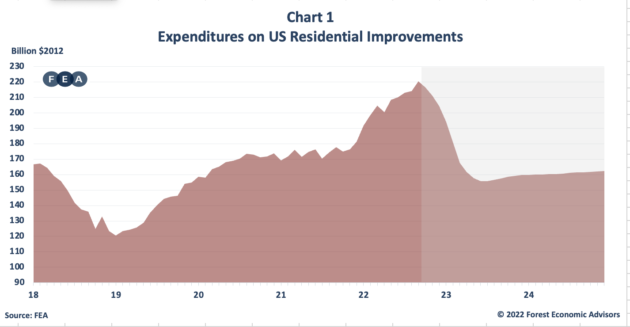

This short-lived downturn in 2023 for all of lumber’s end-use markets, with the exception of industrial production, will be followed by a return to market growth in 2024, FEA forecasts. Residential repair and renovation (R&R), however, is expected to take longer to rebound. To paint a picture, R&R spending rose nearly four per cent in 2021 and an estimated 19 per cent in 2022, but FEA forecasts it will tumble 21 per cent in 2023 (Graph 1). Still, by historical standards, the amount of money that people are expected to spend on residential improvements will remain high. This is because of rising home equity, a lack of new-entry-level and first-move-up homes due to rising unaffordability, and the aging housing stock. On top of this, U.S. homeowners who bought during the pandemic when rates were low are expected to stay in their homes in order to hold onto their low mortgage rates. These factors should cause homeowners to opt to fix up or expand their current homes rather than move and buy more expensive ones.

Source: Forest Economic Advisors

FEA forecasts U.S. residential-improvement expenditures will drop 21 per cent year-over-year to US$163.8 billion in 2023, which will still be well above the US$149.5 billion average of the latter half of the 2010s. This is expected to drop further in 2024 to US$161.0 billion.

U.S. industrial production, on the other hand, is forecast to dip in the first half of 2023 because of rising interest rates and the slowing U.S. economy, before resuming an upward trajectory. This is because the ISM Purchasing Managers’ Index (a leading indicator for the sector) has shown strength for more than two years, indicating industrial production is likely to continue to grow over the near term. Additionally, inventories of manufactured goods are low and need to be restocked. Lastly, FEA expects reshoring of manufacturing as North American companies deal with supply-chain disruptions and the changing geopolitical environment to further bolster industrial production.

Market weakness follows two volatile years. The pandemic spurred governments to drop interest rates, which in turn caused a flurry of home buying and caused lumber prices to skyrocket to record highs as mills struggled to meet demand amid labour shortages and transportation bottlenecks. Lumber prices dropped sharply in 2022 and are expected to fall but remain above historical averages in 2023 due to higher production costs, the need for dealers to rebuild inventories and the expectation for labour and supply constraints to continue to hamper production for the next two years.

FEA believes the decline in lumber prices is nearing its end. Prices are currently below variable costs in several major producing regions, causing some mills in the west to curtail production even as inventories are near record lows. Lumber prices will continue to move up early in the first quarter of 2023 as dealers take advantage of some of the lowest prices in nearly three years to rebuild their depleted inventories. While FEA expects prices to move up initially, the downturn in end-use market activity will cause a substantial decline in lumber prices in the second quarter.

The high prices reached during the pandemic led mills to invest in capacity expansions, which are expected to become operational in 2023. This increased supply will more than satisfy weakening markets and keep downward pressure on prices throughout the remainder of the year. Prices, however, are forecast to be extremely volatile through 2024 as the effects of COVID-19 linger and low stocks force dealers to buy just enough wood to meet their immediate needs at higher prices than they want. This will force prices sharply lower in a cycle that will repeat itself over the next year.

Overall demand for softwood lumber in North America will fall 8.3 per cent to a nine-year low in 2023, following a 1.6 per cent drop in 2022, as end-use markets weaken, and a recession remains likely. This will be short-lived, however, with a 7.5 per cent rise forecast in 2024 at 62.5 BBF.

North American softwood lumber demand is driven by U.S. consumption. In 2021, as prices soared to record highs, U.S. consumption reached a 15-year high. FEA forecasts that U.S. lumber consumption dropped by 0.5 per cent in 2022 and will decrease by another 9.1 per cent in 2023 as end-use market activity deteriorates. This is in response to the U.S. Federal Reserve raising interest rates to slow the overheating economy. Additionally, nonresidential markets are hampered by weak demand for commercial and retail space. However, as those markets improve in 2024, so will U.S. lumber consumption. FEA estimates growth of 8.7 per cent over 2023 to 52.14 BBF.

In Canada, year-over-year lumber consumption fell every quarter from the third quarter of 2021 to the second quarter of 2022, as activity started to decline from the strong year-ago levels. Canadian consumption reversed this trend in the third quarter of this year, and we expect yearly growth will continue through the first quarter of 2023. However, as in the U.S., Canadian domestic lumber consumption will dip overall in 2023 due to rising interest rates. Even with the pickup in end-use markets in 2024, Canadian consumption will fall another 0.9 per cent in 2024.

The recent high prices caused North American offshore exports to drop. A significant reason for this is that exports to China are expected to continue falling in 2022-23. Sanctions imposed on Russia following its invasion of Ukraine will push more Russian lumber to China, decreasing demand for North American-produced lumber. China also imposed new quarantine restrictions on imports of pine lumber from North America, which has dramatically increased the cost of shipping southern yellow pine and SPF lumber there. Finally, strong domestic consumption and relatively high prices will further hamper North American exports to China.

As a result, North American offshore exports will decrease 7.9 per cent in 2023, following a steep 23 per cent drop in 2022. With the expectation for China to ease its restrictions on North American pine we expect offshore exports to pick up 11 per cent.

Paul Jannke is a lumber analyst and principal of the North American wood products analysis and information source, Forest Economic Advisors, LLC (FEA). www.getfea.com.

Print this page