Features

Opinions

Sawmilling

3 ways wood product manufacturers can reduce insurance premiums

There have been steady increases in insurance premiums for the wood product industry since 2012. Will Downing, a CapriCMW Risk Advisor specializing in wood product manufacturing, discusses the biggest concerns for insurance carriers and what you can do to reduce your premiums.

May 6, 2022 By Will Downing

Photo: Annex Business Media

Photo: Annex Business Media The explosions that occurred at the Babine Forest Products and Lakeland Mills sawmills in 2012 resulted in four deaths, over 40 people injured, job losses of industry veterans as well as lengthy investigations and a class action lawsuit. It was estimated to have cost insurance carriers between $25 to $100 million for just one of these claims.

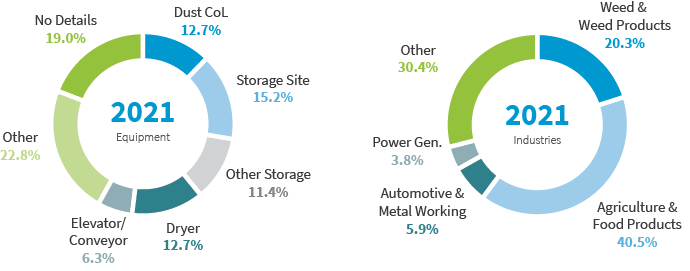

There have been steady increases in insurance premiums for the wood product industry since 2012. According to data collected by Dust Safety Science, the wood and wood products industry was responsible for 20.3 per cent of all industrial fires and known causes were dust collection systems 12.7 per cent of the time.

Industrial Fires – Industries and Equipment Involved. Source: 2021 Combustible Dust Incident Report by Dust Safety Science.

With over $1 million of claims each month in the wood product industry, premiums are continuing to rise and the situation is worsened by the “hard market.”

It is not uncommon to see insurance ratings at $2 per $100 of property value. If you are looking to insure your wood manufacturing property and your buildings are worth $4.5 million, a premium of $90,000 could be expected.

So what can be done to bring your premiums down?

In the case of the Babine Forest Products and Lakeland Mills explosions, the underlying factors that caused the deaths and significant property damage include:

- Ineffective wood dust control measures

- Ineffective inspection and maintenance

- Inadequate supervision of clean-up and maintenance staff

Today, these are some of the biggest concerns for insurance carriers when assessing the operations of wood product manufacturers. It is the responsibility of your insurance broker to advise you on proactive risk management strategies that can help secure better rates and terms from insurance markets. At CapriCMW, our risk advisors provide professional guidance and support on risk management best practices for wood product manufacturing operations, including dust control and mitigation, maintenance and clean-up controls and protocols, and hot work controls.

Aside from keeping your facility clean and organized, well-managed, and reducing hazards, it is important to have documentation of all the measures that you have implemented.

There are three major elements in your presentation to insurance carriers that can help reduce premiums:

- Third party risk inspection

- Documentation and monitoring

- Annual maintenance reports

Having a documented risk management plan, maintenance schedule and clean-up protocol in writing for all to see is critical. Additionally, it is highly recommended that you hire a certified third party to visit the facility and conduction an inspection every three years. While these steps do require additional resources and expenses, the time dedicated to risk control will be worth the investment.

To illustrate the impact, using the $4.5 million building in our example above:

- Without a three-year risk report, documentation on risk management or housekeeping, the premium will likely fall in the $90,000 range.

With a three-year risk report, documentation, and excellent housekeeping, your premium will likely be around $67,500.

To put that into context, a third party risk report and other recommended risk management items may cost annually $10,000-$15,000. However, you could see savings of $22,500 per year or $112,500 every five years in insurance premiums.

Will Downing is a risk advisor specializing in wood product manufacturing at CapriCMW. wdowning@capricmw.ca.

Print this page