Industry News

Markets

News

Abundant supply keeps lumber prices moderated: Madison’s

April 25, 2023 By Madison’s Lumber Reporter

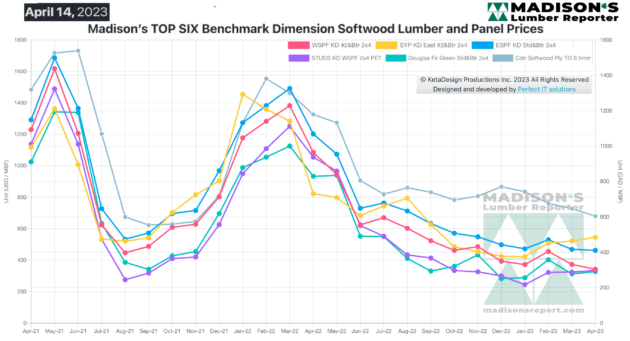

Following the Easter long weekend, demand for lumber increased somewhat however supply remained abundant. Sales to retailers increased noticeably, as weather across the continent became more seasonably mild. Prices of most softwood lumber and panel commodity items remained relatively even; some were up and some were down a little bit. Sales volumes remained lower than historically normal for the time of year. Expectations for the usual spring building season remained — once again — in the future. It seemed like the recent influx of European wood imports was starting to slow down.

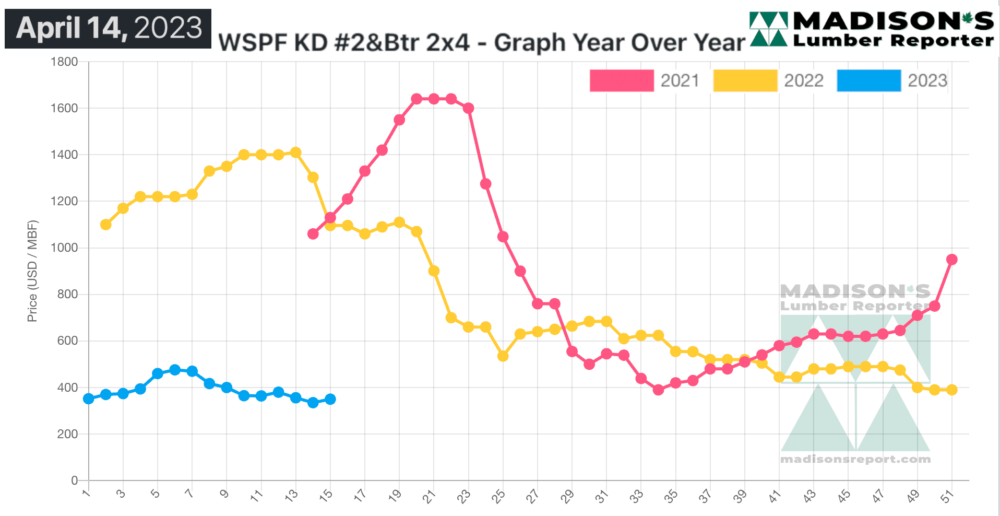

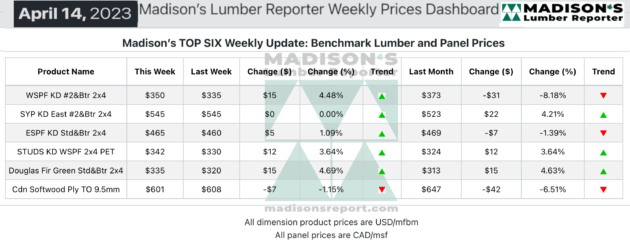

In the week ending April 14, the price of benchmark softwood lumber item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$350 mfbm, which is up by $15 or 4.0 per cent, from the previous week when it was US$335 mfbm. This is down by $23, or 6.0 per cent, from one month ago when it was $373.

Sales of panels continued to flounder compared to lumber and studs, though Oriented Strand Board seemed to gain some traction. Meanwhile, real spring construction and resultant demand for building materials remained elusive.

“Many buyers considered Easter weekend the latest important litmus test, and after seeing steady numbers from the sawmills, decided to secure more coverage.” — Madison’s Lumber Reporter

Advertisement

Sales across the entire North American solid wood commodities market continued to sputter to life, and US Western S-P-F was no exception. Availability appeared abundant as buyers stuck to their hand-to-mouth purchases, but mounting reports of tightening supply at the sawmill level belied the notion of a vastly oversupplied market. Retailers were busier than in recent weeks, noting that the counteroffers accepted by mills have recently slimmed down to $5 to $10 at most. The influx of European spruce seemed to be waning lately, but there was still plenty available at lower price points than domestic wood. Producers maintained two- to three-week order files.

Western S-P-F lumber prices firmed up for the most part as players returned to their desks after the Easter holiday long weekend. While Monday was quiet, sales gained momentum from Tuesday-on. Players continued to report a broad perception of oversupply from the view of buyers, however. While sales volumes showed a promising direction, demand had yet to equalize with supply and reach a pace typically associated with the spring season. Secondary suppliers continued to field good takeaway from buyers looking for last-minute coverage. Two-week order files at sawmills were the norm.

“Buyers of Kiln-Dried Douglas-fir commodities continued to play it cautious, sticking to short-term coverage of their most immediate inventory-needs. Apparently, some sawmills were having trouble restocking on fibre as log sellers boosted their asking prices, and kept shopping around until they found someone willing to go higher on purchase price. For their part, producers upped their asking prices on narrows a jot and held the line on less-popular wides for the time being. At sawmills, dimension lead times were still into the week of April 24th.” — Madison’s Lumber Reporter

Compared to the same week last year, when it was US$1,096 mfbm, the price of Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending April 14, 2023 this price was down by $746, or 68 per cent. Compared to two years ago when it was $1,130, that week’s price is down by $780, or 69 per cent.

Print this page