Industry News

Markets

North American softwood lumber prices continue dizzying reversals

June 25, 2019 By Madison's Lumber Reporter

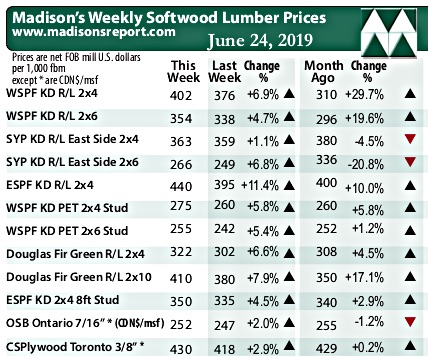

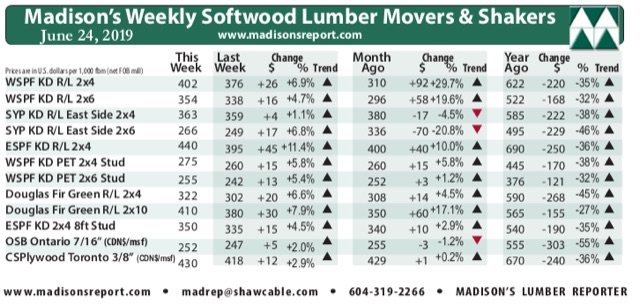

The sheer plummet, then flat-line, of North American construction framing softwood lumber prices for most of this year continued last week the massive reversal of the previous week. Wholesaler prices of benchmark dimension softwood lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr (RL) (net FOB sawmill) last week corrected up somewhat further. The ability of Eastern Spruce-Pine-Fir suppliers to raise their prices significantly confirms the upward price movement of lumber commodities in the past two weeks.

Confusion reigns still; however, Tuesday lumber futures on the Chicago Merchantile Exchange might provide some clarity, as it closed unchanged from Monday’s levels of just below U.S. $400 on the July and September contracts.

Momentum from the previous week’s flurry of demand carried over to generate solid sales volumes last week. — Madison’s Lumber Reporter

The huge (up to 20%) correction upward the previous week continued last week, with benchmark lumber commodity Western Spruce-Pine-Fir 2×4 wholesaler price gaining another +$26, or +7%, to U.S. $402 mfbm, from the previous week when it was U.S. $376 mfbm. This week’s price is +$92, or +30%, more than it was one month ago. Compared to one year ago, this price is down -$220, or -35%.

Be ahead of these data releases … Don’t delay, this week’s softwood lumber market comment was published to the website Monday morning.

* Madison’s Lumber Prices, weekly, are a good forecast indicator of U.S. home builder’s current lumber buying activity

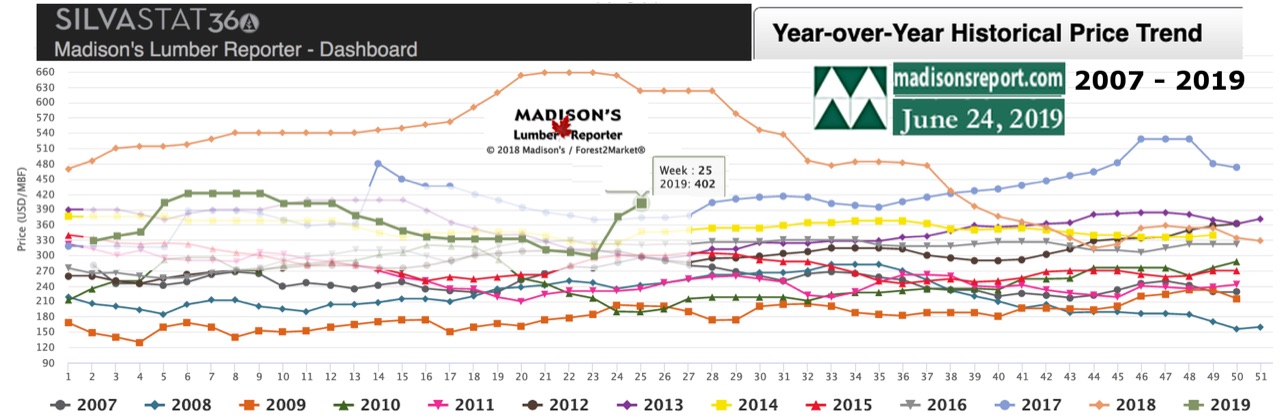

The recovery started two weeks ago has caught up to a good portion of the price drops experienced so far this year. This week’s WSPF 2×4 #2&Btr KD S4S (RL) price is down just -$5, or -1%, relative to the one-year rolling average price of U.S. $407 mfbm. Last week it was +$30, or +8%, higher. The two-year rolling average price is U.S. $451 mfbm.

Overseas markets remained stable, with increased demand from Japan leading to encouraging projections for 3Q sales. — Madison’s Lumber Reporter

Sales activity wasn’t as “crazy” as it was the previous week for purveyors of WSPF lumber in the U.S. However, prices continued to advance and sawmills were definitely in the driver’s seat during negotiations. For their part, WSPF producers in Canada were “sold out” of 2×8 and 2×12 R/L #2&Btr by midweek, with their order files pushing into the week of July 8. Demand continued to ramp up from all over the U.S. and Canada as markets rumbled to life. Rail traffic shouldered increased transit volumes with no problem since sawmill production shutdowns and curtailments have taken so much overall production out of the market. Log decks at lumber manufacturers were fine for the time being.

After “pounding up hard” the previous week, prices of liln-dried fir lumber cooled off marginally last week. Asking prices, though, climbed regardless, by anywhere from $10 to $30. Prices of studs were another story, as production volumes have taken multiple hits from curtailments and shutdowns in recent weeks so sellers were able to bump up levels by quite a margin.

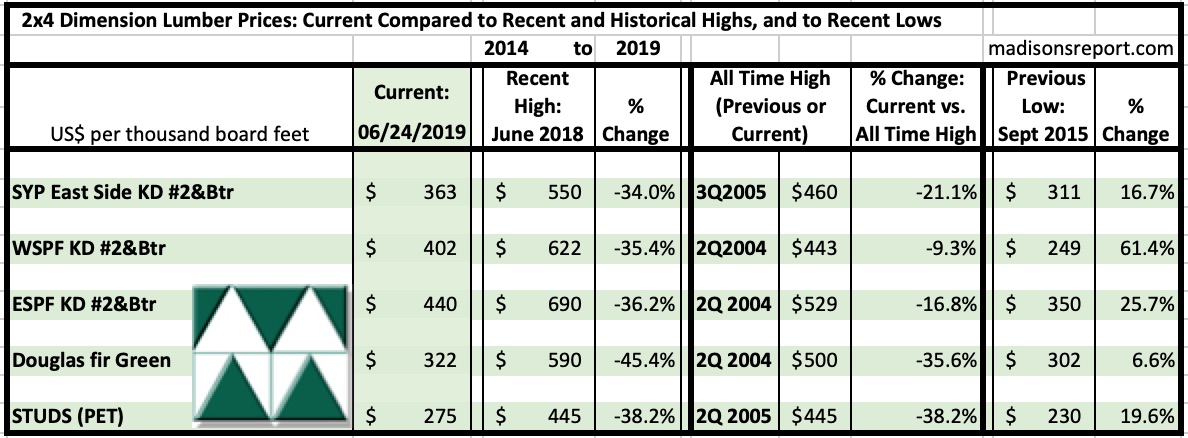

The below table is a comparison of recent highs, in June 2018, and current June 2019 benchmark dimension softwood lumber 2×4 prices compared to historical highs of 2004/05 and compared to recent lows of Sept. 2015:

Print this page