Industry News

Markets

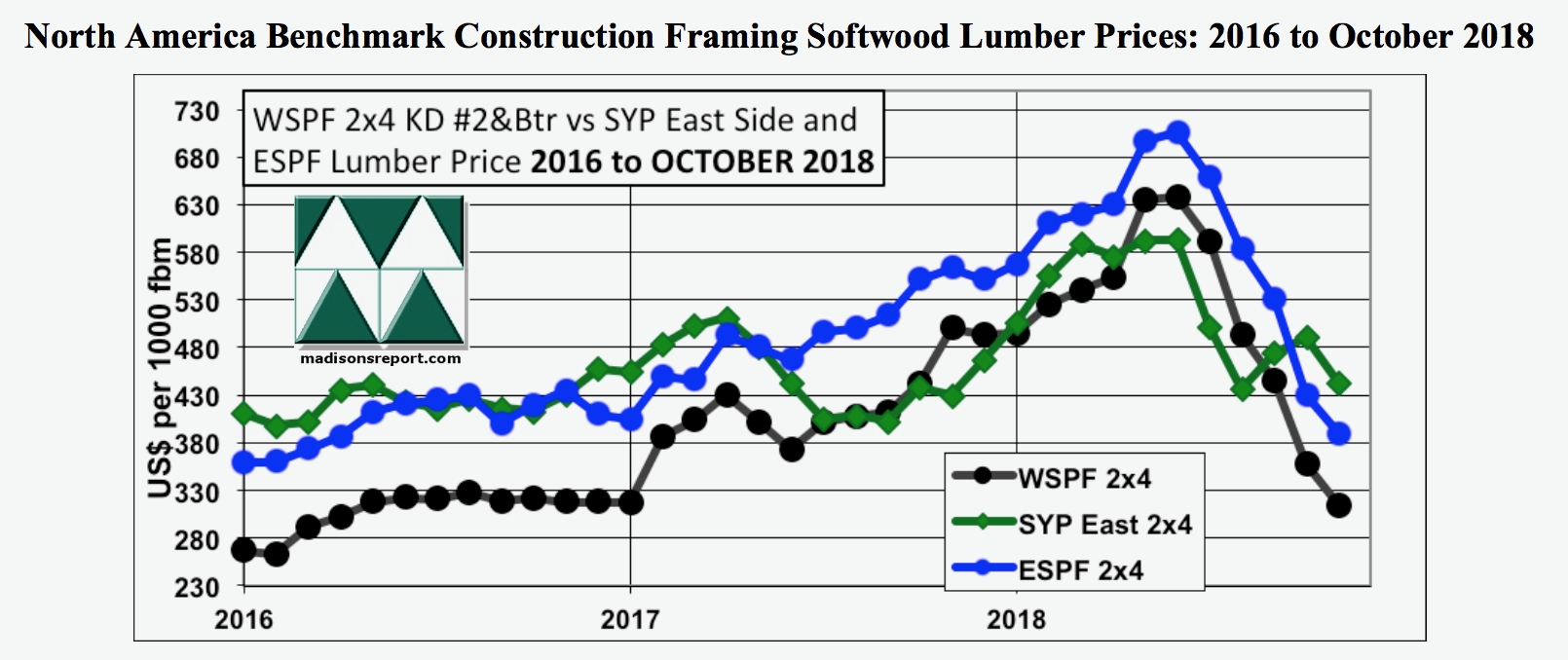

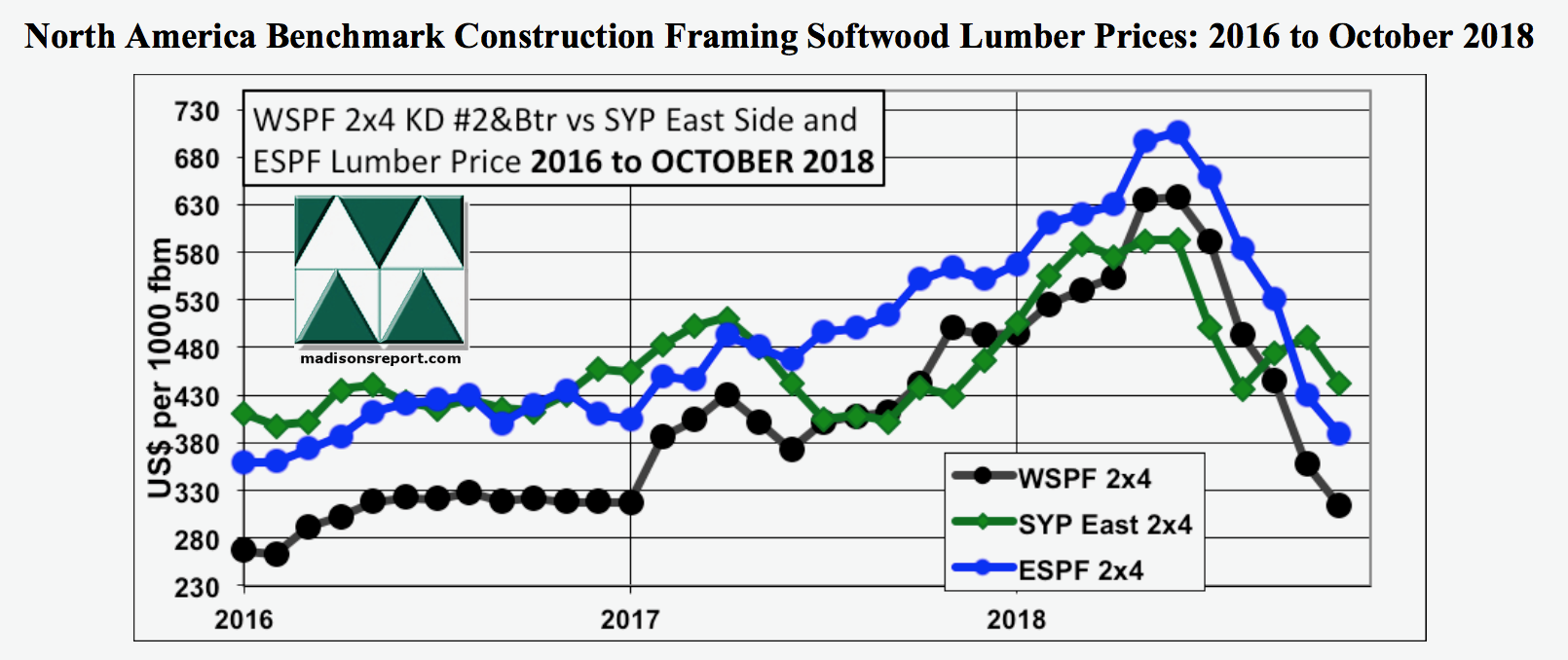

Overview of current North American lumber market

Nov. 21, 2018 - The question at hand: Why there is apparently no price difference between Canadian sales to domestic markets and sales to U.S. export markets?

November 21, 2018 By Keta Kosman Madison's Lumber Reporter

The short answer is: because the Canadian market is too small. These customers do not buy in large enough volumes to be able to influence the direction of prices.

The longer answer is: the established supply chain for the movement of Canadian wood assumes it will be delivered across the U.S. border.

In a “normal” lumber market (high sawmill capacity utilization rates, steady lumber sales, good log supply) the established wisdom has estimated the first 5% – 10% of any softwood lumber duty could be passed on to the customer in the form of higher prices. Any duty rates higher than that had to be paid by the operator.

3Q 2018 Update

So far since this round of U.S. softwood lumber duties were applied on Canadian imports at the start of 2017, producers have been able to pass on the entire duty rate to their customers. Indeed at that time, sawmills were running at high capacity, buyers kept ordering more and more wood, so consequently lumber prices were rising.

This is because demand from the U.S. for real building projects that were currently ongoing was unrelenting, and quite beyond anyone’s expectations. The immediate supply-demand balance was such that sellers were in a good position to force customers to pay the additional duty rate.

For our previous two reports this year, Madison’s found that non-U.S. (Canadian, export) customers who have good, long-established relationships with certain operators, were able to get a “5% to 10% discount” on print FOB mill lumber price. The actual discount was generally acknowledged to be “closer to 6%”.

That remains true in 3Q 2018, however there are other market dymanics and circumstances which have developed. In particular, return-to-trend after a sudden difference in the movement of trendline for Southern Yellow Pine price compared to Western- and Eastern-Spruce-Pine-Fir at the start of 2Q 2017. Madison’s also has details from Canadian remanfucturers on price differences they are quoting for customers in Canada, in U.S., and overseas.

The latest answer to the question of a ‘sans-duty’ or ‘Canadian’ price remains about the same: 6% to 8.5% discount on print for Canadian lumber selling into Canada for those with well-established relationships. Madison’s expects this to change, however, even before the end of this year.

The dynamic of market conditions for North America softwood lumber products, the supply-demand balance if you will, has changed drastically since our last report. Customer purchasing enthusiasm for well the past year or more has evaporated into satisfied digestion-mode.

Wood much-needed and slow to arrive during 2H 2017 and 1H 2018 has long ago been received at it’s destination, and more product subsequently ordered is also on-hand with end-users. As well, there has been a slow-down in U.S. construction activity; which is not surprising given that is normal for the season, and that building was much more robust than expected until the end of 2Q 2018.

At the start of 3Q, suppliers, especially producers, quickly found themselves with bursting inventories – and more manufacturing booked to come online quickly. Buyers, meanwhile, had backed off almost entirely. Prices responded accordingly.

However, a couple of developments have occurred during 2017 and certainly through this year, which give Canadian sawmills, remanufacturers, and exporters new business and new opportunities. Those in British Columbia certainly, as well as other regions, are foregoing conversations with their traditional US customers to wrangle agreements with new business offshore.

“Why wouldn’t we,” they explain. “When we can sell the same wood for more into emerging markets in Asia (or even China)”. This given that US customers right now are still trying to hammer suppliers lower on prices.

Demand from various Asian countries is very hot right now.

In addition, the U.S. is importing higher volumes of wood from Europe this year.

Another variable that has had a shift in dynamic is the sudden increase of U.S. log exports, generally southern yellow pine, specifically to China.

Direct answers from Madison’s sources

• When we ask officially through our weekly survey, sources are horrified and don’t really want to answer (“why are you even asking that!”) so we tread lightly.

• Most players are still using -6% for Canadian pricing for MSR, probably a bigger discount for standard dimension lumber.

• Canadian shipments overseas (Asia) are at a premium to what exporters can get in the U.S., most specifically for HEM/FIR species.

• Through Madison’s queries to lumber traders otherwise, they explain that sawmills provide price lists of differing tallies, from different sales staff, depending on where the wood is going. If a buyer tries to say, “oh I’m sending this within Canada / offshore instead” the supplier changes the price list AND tallies. Thus one can’t exactly compare “apples to apples” as it were. However, once a certain volume is quoted it’s possible to discern a standard increment.

There are several unknowns developing in 3Q 2018: western Canadian players are actively seeking new relationships with customers in emerging markets in Asia; the U.S. is importing higher volumes of lumber from Europe; and, the U.S. is exporting higher volumes of logs to Asia.

In summary

While for the moment there is no relief for Canadian customers of Canadian wood – apart from the small percentage already noted – it is possible this will change before the end of the year.

Indeed, if lumber demand does not pick up again at the beginning of 2019, there will develop a circumstance that even U.S. customers will refuse to take the hit for the duty and will force suppliers to reduce their price quotes accordingly. However, Madison’s expects U.S. wood purchasing for spring construction activity to come back on rather strong in January. It is likely Canadian sawmills have the same opinion. Thus producers will be able to hold off customer counter-offers through the end of this year; usually by scheduling maintenance shutdowns and curtailments throughout their facilities, thereby reducing supply.

Already a few Canadian lumber companies are on the record stating that lumber prices have “found a floor”. The run-up of wood prices this summer is met with an equal drop through September and October. All the sawmills have to do is hang on until the holiday season. By next year, demand from the U.S. will likely be ramping up again.

Meanwhile, the search for new markets and new products (specifically higher-value remanufactured wood) continues. Madison’s will have more information on this exciting development next quarter.

Results

Unexpected hot demand for lumber in the U.S. kept prices high for most of this year. Severe supply-chain issues only exacerbated this situation. Sawmills and lumber suppliers took full advantage of this by raising prices as much as they could. The duty rate into the U.S. was simply added on to seller list prices. Customers were not in a position to negotiate this back down.

As the summer closed and lumber demand in traditional markets dropped, producers turned to new emerging regions in Asia – where demand is very strong. Generally speaking, when traditional customers return to buying, Canadian producers switch back to supplying wood to them. As this year ends and more data comes out, there will be more clarity on this developing market situation. Madison’s is happy to revist this question again next quarter.

Keta Kosman is the editor of Madison’s Lumber Reporter. madisonsreport.com/

Print this page