Industry News

Markets

Recent softwood lumber price volatility settles down, China ports “bursting” with wood

March 20, 2019 By Madison's Lumber Reporter

As delayed data releases out of the U.S. catch up to the usual schedule, recent indications out of China show a sizeable drop in log and lumber imports for full-year 2018. Traders report zero ordering and the ports have been choked with wood — some unsold — for at least a month. Next week the latest data on U.S. home building will be released; by then, all the data sets will be on their usual schedules. Be ahead of these data releases! Don’t delay – this week’s softwood lumber market comment was published to the website Monday morning.

China lumber import volumes: full-year 2018

Official data out of China can often be not an accurate representation of a particular situation. In manufacturing, it is often possible to reasonably validate data with other metrics; for example, to correlate official Manufacturing Index trends against energy consumption data. Such comparison for wood products is difficult, because a lot of that material in China goes into other uses than building. So it is difficult to get true figures on lumber consumption, as it is in the U.S. and Canada.

However, all accounts at the China ports that Madison’s is aware of are: “Customers won’t even take quotes, ports at bursting with stock.”

Softwood lumber sales quieted down further this week; transportation issues and pockets of bad weather persisted in many key wood-consuming markets. — Madison’s Lumber Reporter

Advertisement

With producers, for sawmills in Canada and the U.S., this was “another digestion week,” as mills maintained reduced production volumes and stood pat on most of their asking prices. The lion’s share of buyers took a break from the market and waited for delayed loads ordered in previous weeks to arrive.

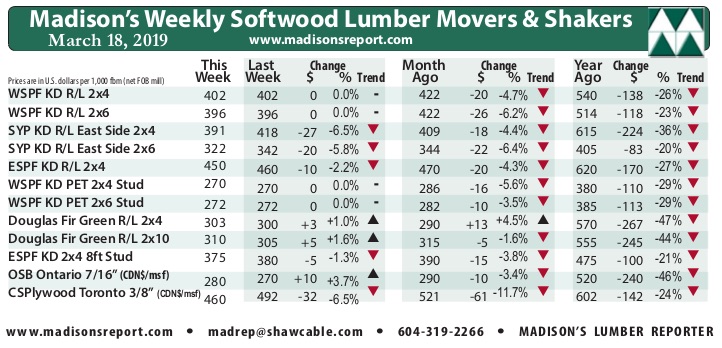

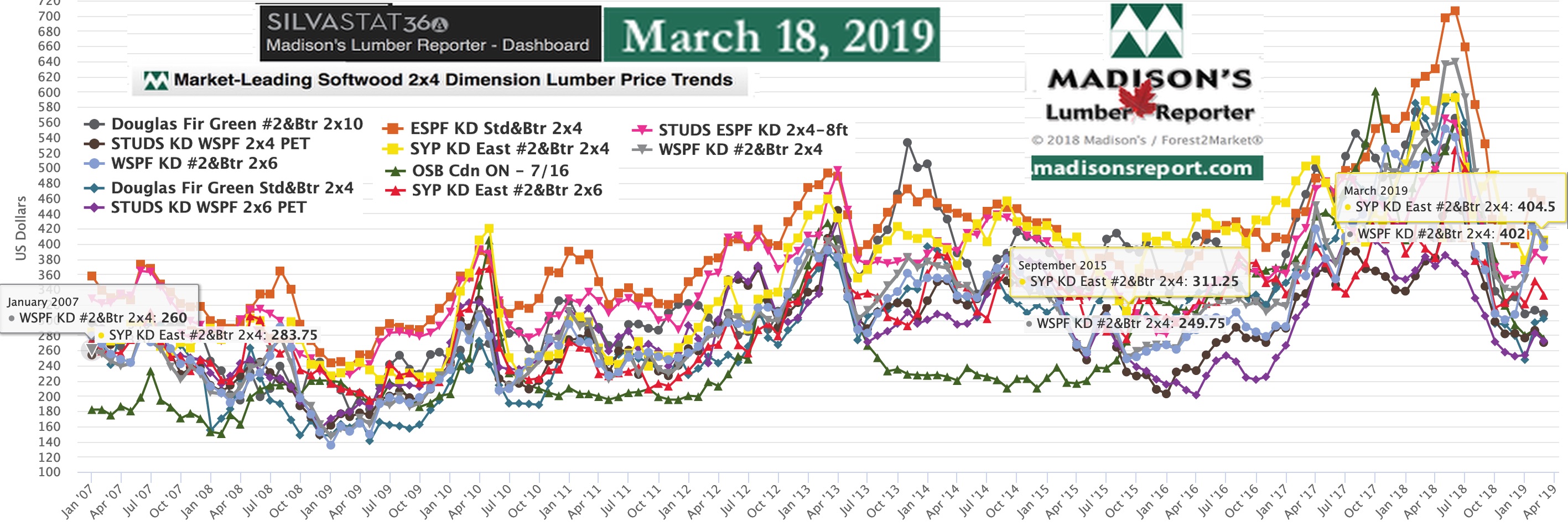

Now that lumber prices have moderated to a new “normal,” Madison’s took a look back over the recent past for the lowest level. Print Friday by Madison’s Lumber Reporter on benchmark Western Spruce-Pine-Fir KD 2×4 #2&Btr (wholesaler price, net FOB sawmill) was unchanged from the week before, at U.S.$402 mfbm. This is -5% lower than in mid-February when that price was $422, and a -25% drop from one year ago’s U.S.$540 mfbm.

By comparison, the recent high for WSPF 2x4s, in June 2018, was U.S.$550 mfbm.

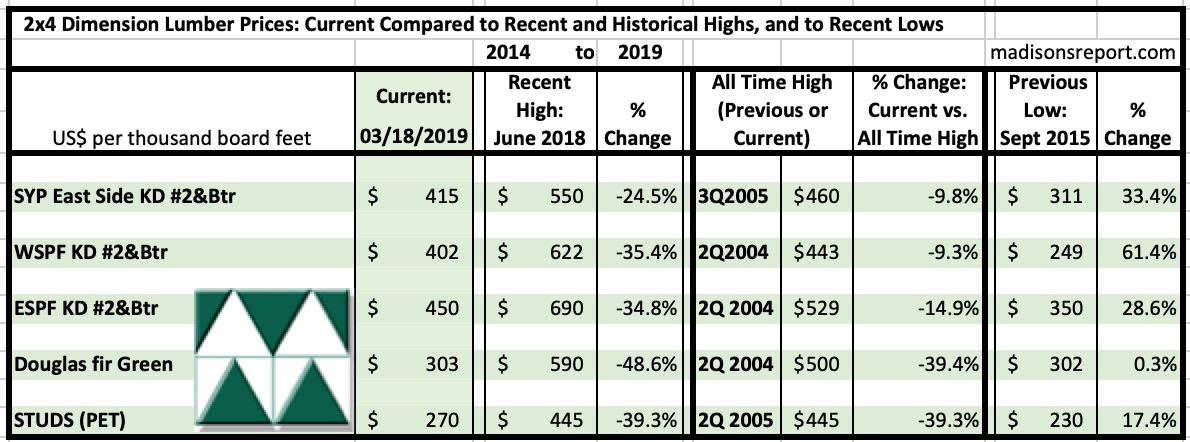

The below table is a comparison of recent highs, in June 2018, and current March 2019 benchmark dimension softwood lumber 2×4 prices compared to historical highs of 2004/05 and compared to recent lows of Sept. 2015:

There was improvement with weather in some important home building markets, but large parts of the U.S. and Canada remained frozen or were sopping from recent rains and snowmelt. Transportation, as usual for the past couple of years and always during this season, was plagued with problems which delayed already late shipments.

Given the robust inventories at both supplier yards and secondary resellers, customer interest in new buying was low. Sawmill order files were quite soft for this time of year.

Producers sat on two week order files and felt no pressure to churn out more lumber, especially in view of Western Forest Products’ announcement that their Alberni Pacific Division Sawmill will be shutting down for a full month starting March 18. — Madison’s Lumber Reporter

As winter draws to a close across North America, there is potential for some big spring storms. Since last week, massive parts of Nebraska are under water and it is expected to be a while before those cities dry out. At least one functioning bridge collapsed under the sheer volumes of water and ice. Rebuilding from these kinds of climate impacts will be just as important as new building this coming U.S. and Canadian construction season.

Print this page