Ongoing harsh winter weather at the start of the year has put a dampening effect on construction activity across the continent, thus on lumber sales. Prices of lumber have responded accordingly.

In February there was some strength to demand resulting in price moving upward, but this level dropped down in the beginning of March.

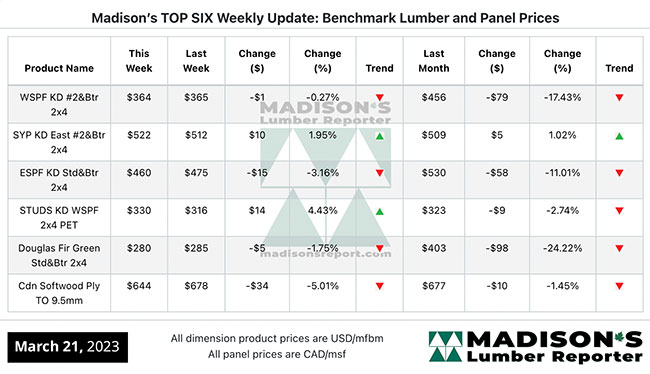

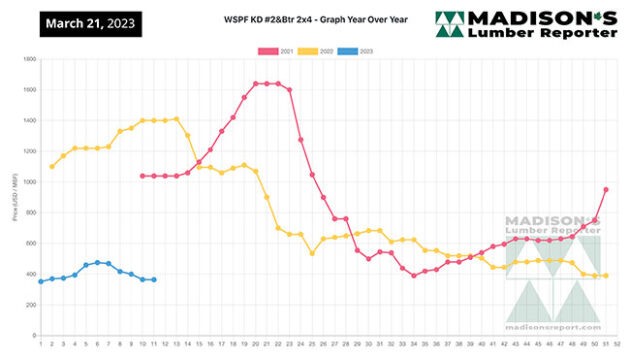

Waffling up then down this year so far, in the week ending March 3, the price of benchmark softwood lumber item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$400 mfbm, which is down $17 or 4.0 per cent from the previous week, when it was $417 mfbm. This is down by $56, or 12 per cent, from a month ago when it was $456.

Compared to the same week last year, when it was $1,330 mfbm, the price of Western S-P-F 2x4s was down by $930, or 70 per cent. Compared to two years ago when it was $1,040, that week’s price is down by $640, or 62 per cent.

Due to this late-arriving spring, customers were only covering short-term needs and filling holes in their inventory. Most were not stocking up on supply, preferring instead to hold off purchasing to see if prices would drop further.

Sawmill order files remained at about two weeks at most facilities in the West and were out to about three weeks in the East. There was plenty of inventory in the field, so customers felt no urgency to buy. Indeed, some secondary suppliers were offering such discounts – just to make sales – that they sold below current replacement costs.

Expectations are for a shorter building season this year than has been in the previous three years. As such, when spring does finally arrive there could be a brief run on lumber sales, with prices popping up in response, followed by a lull as summer comes on.

As for the all-important housing market, in 2022 the U.S. began building 1.55 million homes, just a three per cent drop from full-year 2021. Single-family starts in 2022 totalled 1.01 million, down 10.6 per cent from the previous year. The latest data available for January 2023 shows starts down slightly compared to December, which is normal for the time of year.

However, permits for both total and single-family are essentially flat. This after a big jump of 11 per cent for single-family permits in December. Building permits are generally submitted two months before construction begins, so this explains the expectations for a burst of home building activity come April and May.

Housing completions posted a 1.0 per cent annual gain, rising to an estimated annual rate of 1.406 million housing units. Continuing the drops of recent months, there were 1.673 million units under construction. Of those, 752,000 were single-family homes, compared to 769,000 in December 2022.

January data showed sales of new single-family homes in the U.S. increased for the fourth month in a row, at 670,000 units, which is up more than 7.0 per cent from December’s upwardly revised 625,000 and is a 19 per cent drop compared to January 2022 when it was 831,000 units.

Houses under construction accounted for 52 per cent of the inventory sold, with homes not started making up 26 per cent. Completed houses accounted for 23 per cent of the inventory, a big improvement from 15 per cent the previous month.

The trend line of panel prices is often a good forward indicator of what could be coming for dimension lumber. In the week ending March 24, Canadian softwood plywood 3/8” FOB Toronto was C$644 msf, down by $34, or 5.0 per cent, from the previous week when it was $678, and is down by $33, or 5.0 per cent, from one month ago when it was $677.

For it’s part, OSB 7/16” Ontario was flat from the previous week at $340 msf and down only $5, or 1.0 per cent, from one month ago when it was $345.

These levelling-off plywood and OSB prices could suggest that as true spring construction weather finally comes on across North America, dimension lumber prices might also start to flatten out. At what level? Will the 2023 trend for softwood lumber prices be around the $500 mark, or higher?

Given that the historically lowest-price time of year, in the depths of winter and around year-end, has just gone by; there is a good possibility that the spring price level for softwood lumber will be higher than it is at the end of March. Only the next month or two will tell.

Keta Kosman is the owner of Madison’s Lumber Reporter, a premiere source for North American softwood lumber news, prices, industry insight, and industry contacts.

Print this page