Features

Harvesting

Logging Profiles

Survey Snippet #11 – Logging’s next gen

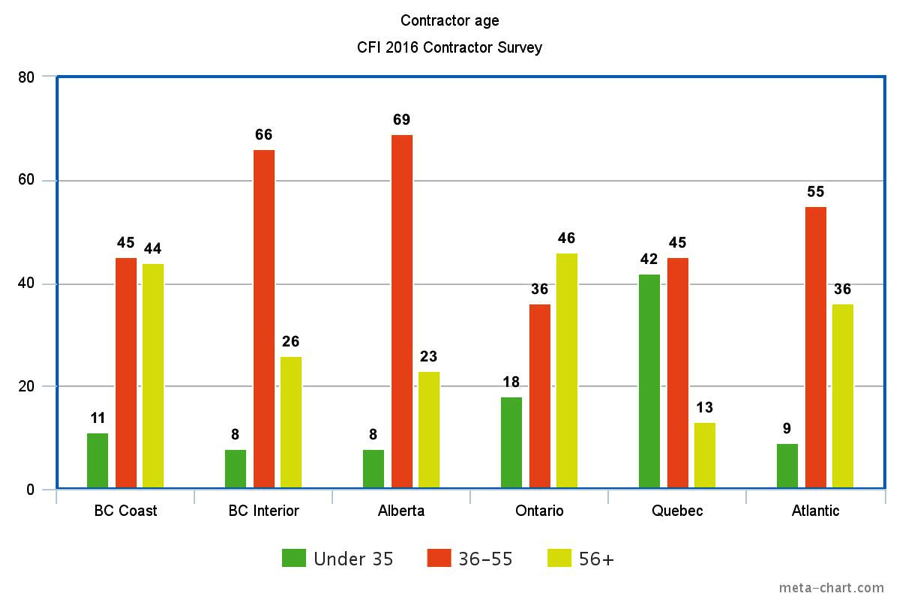

Aug. 29, 2016 - The accepted wisdom is that Canada's logging workforce leans to the older side, with succession planning a major issue facing the industry over the next five years. On average, that may be true, but to a great extent it depends on company size and, more importantly, location. The larger the company, the more demographics and succession are challenges. But above all else, the industry in Ontario and the BC Coast face the largest demographic challenges over the next five years.

August 29, 2016 By Scott Jamieson

Overall, the bulk of respondents are in the 36 to 65 year-old age range, with 56 per cent being over 46 years old. Only 14 per cent are in the 26 to 35 year range. When asked how long they expected to stay in the industry, the results were quite varied. Just over a quarter (28%) expect to be out of the industry in fewer than five years, with an additional 29 per cent expecting to be out in fewer than 10 years.

That 57 per cent is what keeps mill woodlands staff up at night, but there are a lot more sleepless nights for those on the BC Coast and Ontario than elsewhere. On the BC Coast for example, almost half (44%) of contractors are over 56 years old, while another 23 per cent is between 46 and 55. That compares to only 31 per cent over 56 years old in the Interior and 23 per cent in Alberta. In Ontario, however, 46 per cent of contractors are over 56 years old.

To see a succession in full swing, drop by Quebec, where the industry seems to be doing something right. There, only 13 per cent of respondents were over 56 years, while a staggering 42 per cent are under 35 years old. That compares to just 8 per cent under 35 years old in the BC Interior, 11 per cent on the BC Coast, and 9 per cent in Atlantic Canada, where the bulk of contractors are between 36 and 55 (54%) and 36 per cent are over 56 years old.

Not coincidentally, Quebec contractors tend to be small than those in Ontario and western Canada, which may be part of the answer for the younger skewing on demographics. It is easier for younger contractors to start up when the average harvest is well below 100,000 m3 and companies own one or two machines. Still, harvest levels per contractor are only slightly bigger in Ontario and actually smaller in Atlantic Canada, so clearly there is more going on behind these numbers.

Next week Survey Snippet #12 looks at the succession plans of today’s contractor, and what each region may have in store for the coming years.

Missed the last Survey Snippet #10 on fleet replacement plans? See it here.

Find more news for the CFI 2016 Contractor Survey on www.woodbusiness.ca and in our enews in the coming months, with a final digital report in late September and a summary in the Sept/Oct print issue. Be sure to subscribe to the enews to get every item.

The survey was conducted in April 2016 for Canadian Forest Industries by independent research firm Bramm & Associates, generating over 230 replies to a detailed list of questions. Respondents were distributed according to the geographic breakdown of the forest industry, with 50 per cent in Western Canada, 25 percent in Quebec, and the rest found in Ontario, Atlantic Canada, and central Canada. Within BC responses were almost evenly split between the BC coast and Interior. Many thanks to our sponsors for making the research possible – Hultdins, Stihl, Tigercat and Ponsse. Also made possible with support from the Ontario Media Development Corporation (OMDC).

Print this page