Industry News

Markets

Traders abandon offices for summer holidays as lumber prices slip further downward

July 23, 2019 By Madison's Lumber Reporter

An incomprehensible North American construction framing dimension softwood lumber market became no more understandable this week as prices on several key commodities fell further. As Quebec enters its usual two-week sawmill and construction curtailment and true summer weather arrived across the continent, lumber traders abandoned sales offices for local fishing holes and other outdoor activities.

One must congratulate the major sawmills in the Pacific Northwest for such quick response to badly softening prices. Without some serious reductions in supply, prices could have continued falling to below $300 mfbm. While it’s true that right now sales are slow, this is still better in the long run than accepting lower and lower prices to close a deal. Specifically because the latest data of U.S. housing starts, released last week for June, are encouraging. Single-family unit starts are up +3.5% compared to May. More importantly, builders and contractors are reporting a dangerous lack of skilled labour throughout Canada and the U.S. This means construction companies have building projects already planned but not the workers to complete.

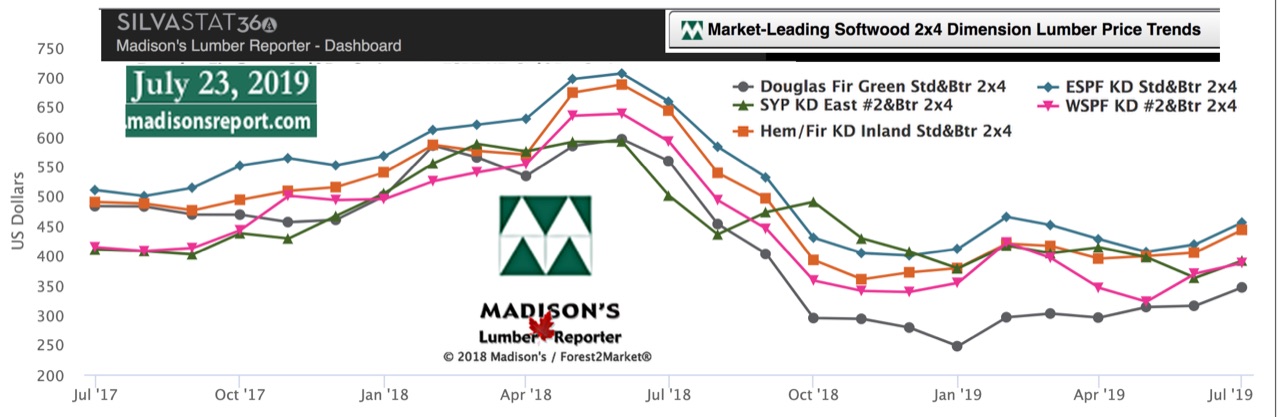

Expectations for the next couple of years are, therefore, that demand for wood will continue at least at the same volumes it has been since 2017.

The volumes of manufactured wood taken out of supply by the downtime and curtailments at many of British Columbia’s largest operators during 2Q and 3Q 2019 prevented a serious depression in pricing. — Madison’s Lumber Reporter

Advertisement

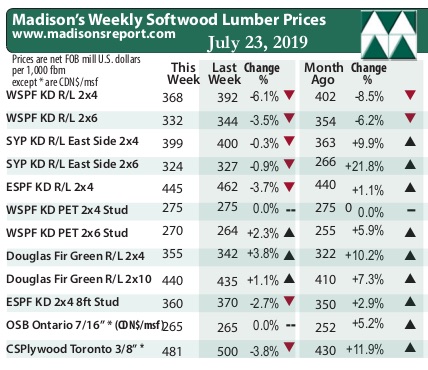

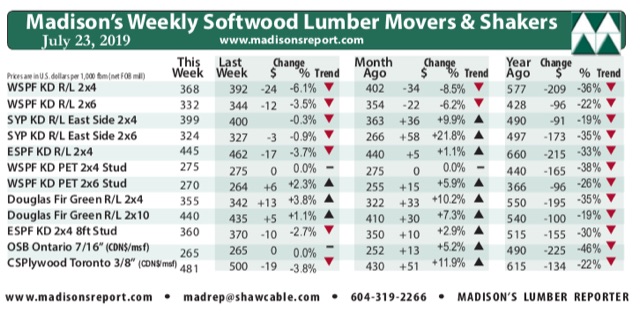

Wholesaler prices sank further on many key lumber commodities, with benchmark item Western Spruce-Pine-Fir KD 2×4 #2&Btr at U.S. $368 mfbm this week, which is down a whopping -$24, or -6.1%, compared to last week when it was U.S. $392 mfbm. This week’s price is -$34, or -9%, less than it was one month ago. Compared to one year ago, this price is down -$209, or -36%.

Be ahead of these data releases … Don’t delay, this week’s softwood lumber market comment was published to the website Monday morning.

* Madison’s Lumber Prices, weekly, are a good forecast indicator of U.S. home builder’s current lumber buying activity

Compared to historical trend, this week’s WSPF KD 2×4 #2&Btr prices are down -$21, or -5%, relative to the one-year rolling average price of U.S. $389 mfbm and down -$83, or -18%, relative to the two-year rolling average price of $451. This week’s price is down -$4, or 1%, relative to the five-year rolling average price of $372.

Players indicated tight field inventories, yet overall buying activity remained quiet. — Madison’s Lumber Reporter

Sellers of WSPF lumber in the United States navigated another week of waffling consumer confidence, down-limit lumber futures, and muted demand. Producers reported short order files, typically no further out than one or two weeks. Buyers apparently had waning inventories but enough to keep feeding burgeoning construction markets.

Sales activity was a bit sloppy last week according to Canadian WSPF producers. The U.S. market was “stagnant.” In Canada it was better, but was not able to pick up the slack left by the former.

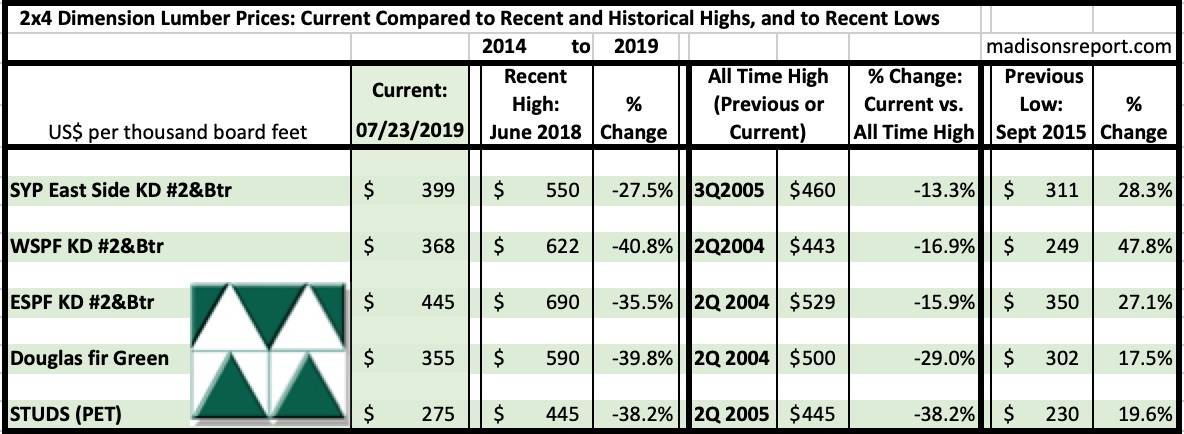

The below table is a comparison of recent highs, in June 2018, and current July 2019 benchmark dimension softwood lumber 2×4 prices compared to historical highs of 2004/05 and compared to recent lows of Sept. 2015:

Print this page