Industry News

Markets

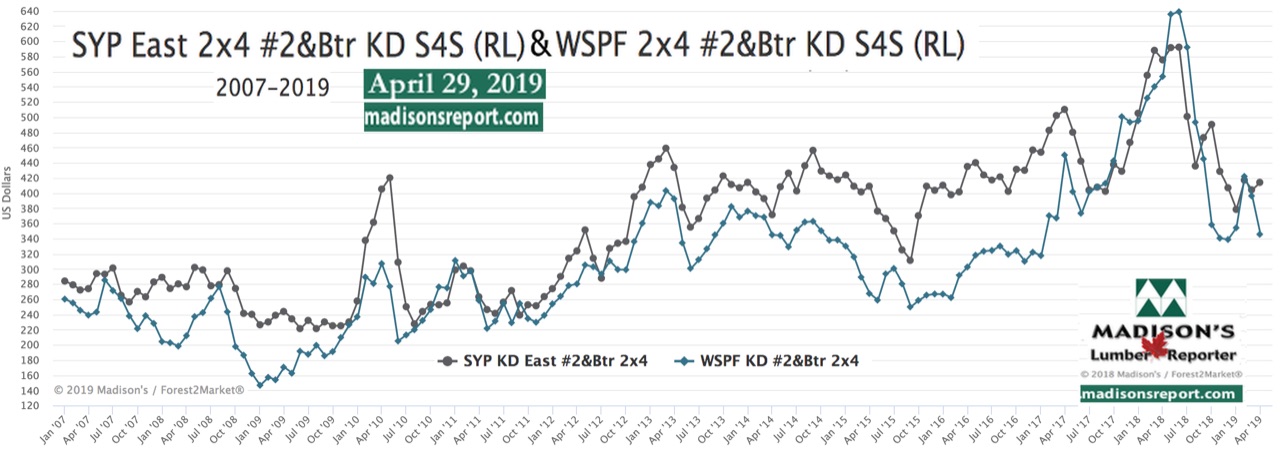

Softwood lumber price recent drops lessen; US home sales, house prices improve slightly

May 1, 2019 By Madison's Lumber Reporter

While North America construction framing softwood lumber prices dropped a bit more last week, the decreases were much less than in previous weeks. Lumber prices did fall, but by a smaller amount than in recent weeks. New data releases for U.S. pending homes sales and house prices, February and Q1 2019, respectively, show slight improvements. In the middle of last week, two major British Columbia sawmill companies announced significant curtailments through May. This news hit a floundering lumber market — one where neither buyer nor seller can be sure of the current supply-demand balance — with a shock that sent undecided customers straight to the ordering table.

Be ahead of these data releases! Don’t delay, this week’s softwood lumber market comment was published to the website Monday morning.

* Madison’s Lumber Prices, weekly, are a good forecast indicator of U.S. home builder’s current lumber buying activity

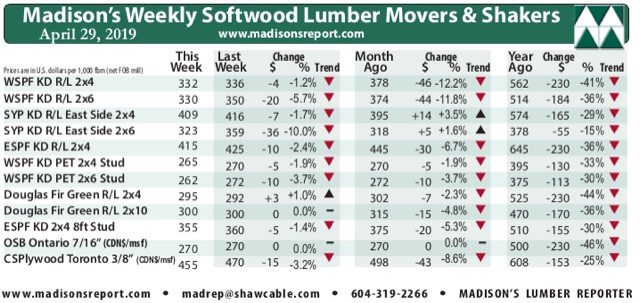

Potentially worrisome, however, was the large drop in Western Spruce-Pine-Fir 2×6 prices, down a full $20 this week, to U.S. $330 mfbm. This size is most-often used in larger homes and especially multi-family construction, so it will be interesting to see what data comes out for that sub-sector of U.S. home building in a couple of months.

For the week ending April 26, 2019, Western Spruce-Pine-Fir KD 2×4 #2&Btr (RL) FOB sawmill wholesaler prices averaged U.S. $332 mfbm, a decrease of -$4, or -1.2%, from the previous week. This week’s price is -$46, or -12%, less than it was one month ago when it was U.S. $378 mfbm. Compared to one year ago, prices are down -$230, or -41%.

Sweeping curtailments by two major British Columbia lumber producer generated some much-needed demand. — Madison’s Lumber Reporter

In the Pacific Northwest, solid wood purveyors said the midweek sawmill curtailment announcement “tipped the lemmings into the abyss.” Just as sales of spruce lumber took off resoundingly, business for kiln-dried Douglas-fir lumber sellers was definitely “way better” than in previous weeks. Sawmills were able to capitalize and extend their order files out to either May 6 or 13. Some KD Douglas fir studs orders were out as far as May 20.

Log prices remained “punishing” for mills, who coped for the past few months by ephemerally jacking up prices whenever there was a whiff of business, which promptly snuffed out any sales potential momentum. This time players wondered if the combination of improving spring construction activity and reduced supply from curtailments might be enough to keep the ball of sales rolling.

Softwood lumber producers in the U.S. reported sawmill order files up to three weeks out after the midweek sales flurry, although dribs and drabs of certain items were still available for the coming week. In Canada, sawmill order files were “definitely extended” after a few days of high sales volumes, but producers couldn’t give exact dates until they sorted through all their new bookings. — Madison’s Lumber Reporter

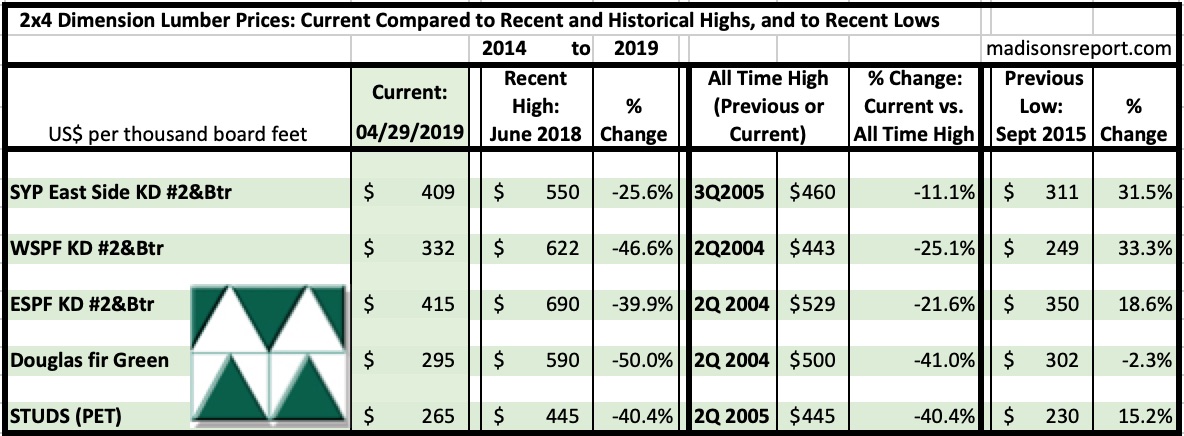

The below table is a comparison of recent highs, in June 2018, and current April 2019 benchmark dimension softwood lumber 2×4 prices compared to historical highs of 2004/05 and compared to recent lows of Sept. 2015:

Print this page