Features

2023 Softwood lumber market year-end update

December 5, 2023 By Keta Kosman

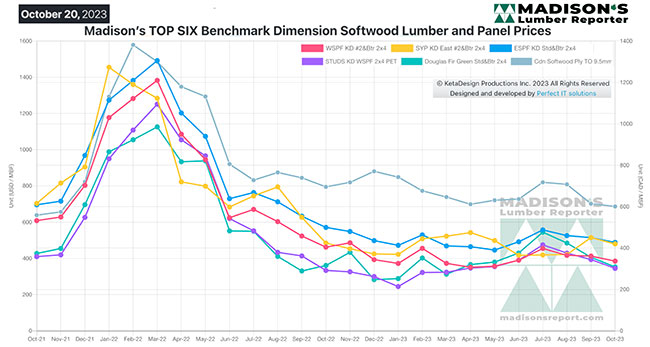

Figure 1. Madison’s TOP SIX Benchmark Dimension Softwood Lumber and Panel Prices

PHOTOS and GRAPHS: All figures courtesy Madison’s Lumber Reporter

Figure 1. Madison’s TOP SIX Benchmark Dimension Softwood Lumber and Panel Prices

PHOTOS and GRAPHS: All figures courtesy Madison’s Lumber Reporter

Toward the end of October, North American softwood lumber prices began their usual annual seasonal drop. Customers, whether retailers or end users, continued to make purchases for immediate needs only, keeping inventories quite lean. Sawmills kept production volumes tight to stay in line with weakening demand as this winter season truly comes on. After the volatility of the previous two years, these more normal price fluctuations were welcomed by industry players. Now that the previously unimaginable price highs are relegated to history, builders and lumber producers are better able to gauge what might come in 2024.

The price high for Western SPF 2x4s this year was US$476 mfbm in the week of Feb. 9, then was $458 for most of July; while the low was in the beginning of January at $370, which is very close to the current price. This more usual price swing of approximately $100 mfbm throughout the year is much closer to what sellers and customers were accustomed to in the past. This means they can more confidently make their business plans for the near future, specifically spring building season 2024.

For the week ending Oct. 20, the price of benchmark softwood lumber item Western SPF 2×4 #2&Btr KD (RL) was US$374 mfbm, down $8 or two per cent compared to the previous week when it was $382. That week’s price is down $39 or nine per cent from one month ago when it was $413.

Compared to the same week last year, when it was $445 mfbm, the price of Western SPF 2×4 was down $71 or 16 per cent, and down by $221 or 37 per cent compared to two years ago when it was $595.

Western SPF traders in the U.S. noted that sawmills drew a line in the sand toward the end of October, especially regarding what they were willing to entertain in terms of counters. While some buyers backed off, accepting this might be the price bottom, plenty others continued to run their meagre field inventories down to bare pavement rather than capitulate. Order files at sawmills slowly stretched into November, making the waiting game a less appealing course of action.

Demand continued to limp along for Western SPF lumber, according to suppliers in western Canada. Takeaway in the field remained soft, as cooler weather further dampened overall demand. Sawmills reported strong counter offers requiring review on a case-by-case basis, with order files stuck at less than two weeks in most cases. Buyers maintained lean field inventories and mostly covered their needs through the distribution network via LTL and mixed load orders. Eroding prices and weak sales increased chatter regarding potential curtailments to bring supply more in line with anemic demand.

The U.S. Thanksgiving long weekend usually marks the beginning of true slowdown for construction activity across the continent, thus for lumber manufacturing as well. Looking back over this year’s rather stable trendline for price changes, the expectation for next year is a continuation of this more “normal” cycle.

The Madison’s Lumber Prices Index for the week ending Oct. 20 was $402 mfbm. This is down two per cent or $9 from the previous week when it was $411.The new formulation having existed for 14 months, Softwood Lumber Futures, as traded on the Chicago Mercantile Exchange, dropped from a high of $578 mfbm in mid-July to $488 toward the end of October.

After spiking to unsustainable highs during the disruptions to society in the past couple of years, U.S. housing starts trended further downward in August 2023. Permits for authorizations of new home building increased, however. Demand for new construction has been boosted by an ongoing acute shortage of previously owned homes on the market. Realtors estimate that housing starts and completion rates need to be in a range of 1.5 million to 1.6 million units per month to bridge this inventory gap. Expectations among construction industry insiders and financial lenders alike is that single-family construction starts could rebound in the coming months, if builders are able to keep their skilled labour.

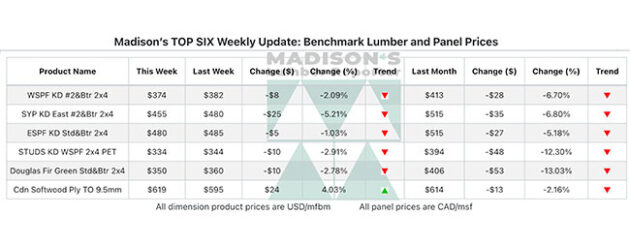

Figure 2. Madison’s TOP SIX Weekly Update: Benchmark Lumber and Panel Prices

Coming off real highs in the previous two years, August total housing starts in the U.S. fell 11 per cent from the previous month to 1.283 million units compared to the 1.447 million units reported for July 2023, and were down 15 per cent from the August 2022 rate of 1.505 million units.

Building permits meanwhile, as an indicator of construction activity to come, continued a recent rising trend to increase by almost seven per cent at 1.543 million units from the July rate of 1.443 million. This is three per cent below the August 2022 rate of 1.586 million. These permits will eventually become starts and will help to underpin residential construction.

August starts of single-family housing, the largest share of the market and construction method, which uses the most wood, dropped slightly, down four per cent to a rate of 941,000 units, from July’s 983,000 units. Single-family authorizations were at 949,000 units, which is two per cent above the July figure of 930,000 units.

Now that the severe volatility and series of extreme circumstances are in the past, the construction and the forest products industries can both use the sales volumes and price data of 2023 to better make their business plans for next year. As the underlying dynamics of the housing market unfolds – not enough homes for the demographic currently reaching home-buying age – expectations are for an uplift in home building next year. Given the ongoing slowdowns and curtailments at sawmills over the past more than one year, there is enough lumber manufacturing capacity able to come online to serve this need.

Keta Kosman is the owner of the weekly Madison’s Lumber Reporter. Established in 1952, Madison’s Lumber Reporter is your premiere source for North American softwood lumber news, prices, industry insight, and industry contacts.

Print this page