Industry News

Markets

Lumber industry hoping for improved sales in September

August 27, 2019 By Madison's Lumber Reporter

All thoughts were on Labour Day and the final throes of summer 2019 last week, as North American construction framing softwood lumber sellers were able to hold firm on pricing for most solid wood commodities. Many players were out-of-office enjoying this waning August. Following a very confusing U.S. home building season, which saw significant curtailments and down-time at several large British Columbia sawmills, the supply-demand balance has corrected.

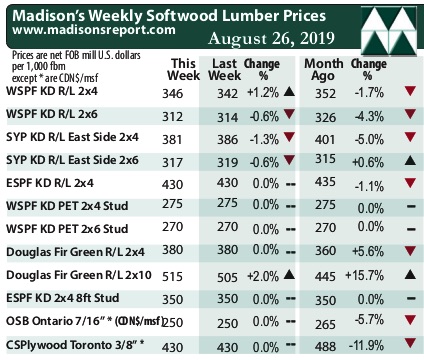

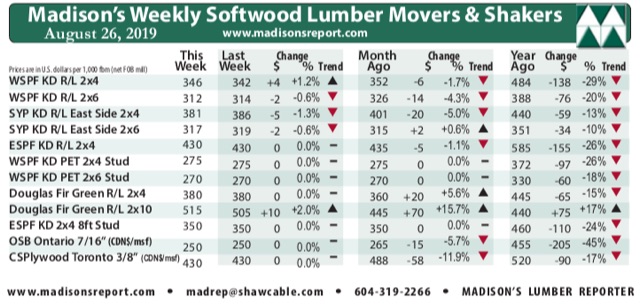

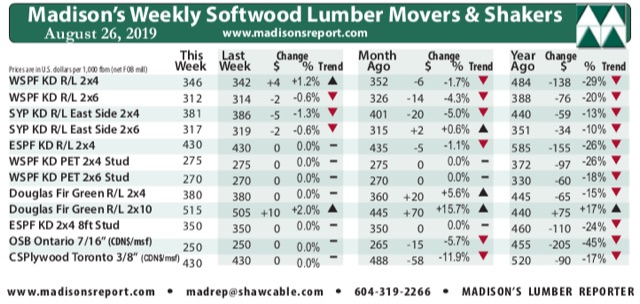

The price of benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr last week gained $4, or 1.2%, to close the week at U.S. $346 mfbm compared to $342 the week before. This week’s price is -$6, or -1.7%, less than it was one month ago. Compared to one year ago, this price is down -$138, or -29%.

Sales volumes were steady in Spruce-Pine-Fir, and encouraging in Douglas-fir, but weak with all other commodity groups. — Madison’s Lumber Reporter

Be ahead of these data releases … Don’t delay, this week’s softwood lumber market comment was published to the website Monday morning.

* Madison’s Lumber Prices, weekly, are a good forecast indicator of U.S. home builder’s current lumber buying activity

Compared to historical trends, this week’s WSPF KD 2×4 #2&Btr prices are down -$25, or -7%, relative to the one-year rolling average price of U.S. $371 mfbm and down -$102, or -23%, relative to the two-year rolling average price of $448. This week’s price is down -$26, or -7%, relative to the five-year rolling average price of $372.

Lumber producers pushed sawmill order files into early September on most items. While stud prices remained firm at levels from the previous week, mills found success with higher asking prices on a few dimension items. — Madison’s Lumber Reporter

Lumber sales and construction activity continued to pick up last week in the U.S. Northeast. This encouraged vendors, who were sick of “beating each other up for orders.” Lumber yards in the region pushed hard to clear out stagnant inventory volumes, which had been built up from June and July. Sales of green Douglas-fir 2×10 and KD 2×4 were standouts; but due to lack of supply, not a surge in demand.

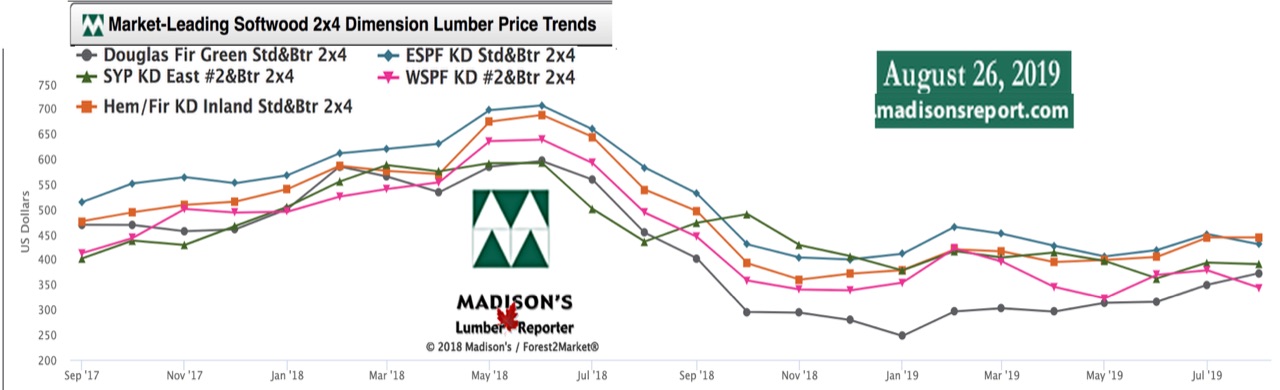

The below table is a comparison of recent highs, in June 2018, and current Aug. 2019 benchmark dimension softwood lumber 2×4 prices compared to historical highs of 2004/05 and compared to recent lows of Sept. 2015:

Print this page