Industry News

Markets

Uneven lumber market as customers seek alternative items

April 7, 2021 By Madison's Lumber Reporter

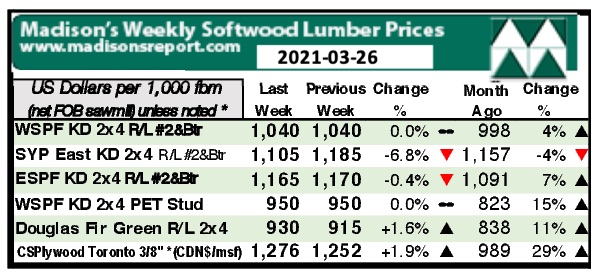

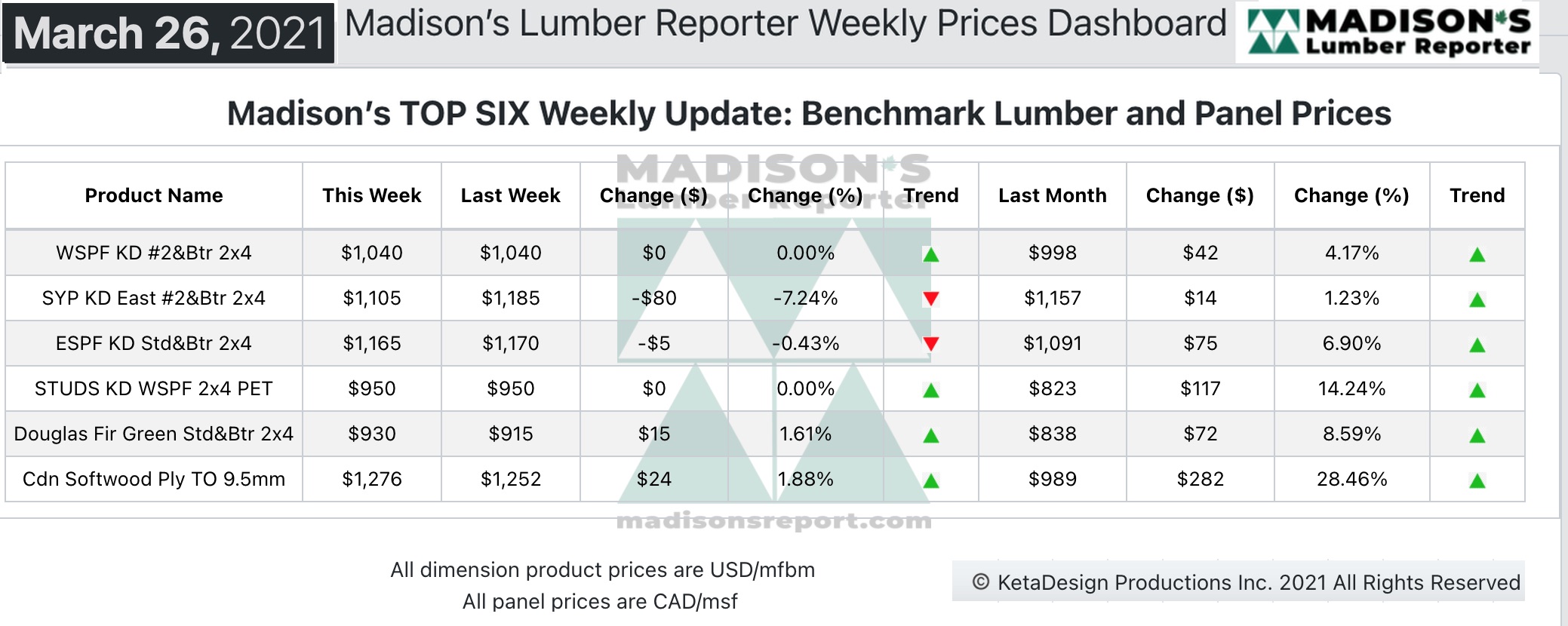

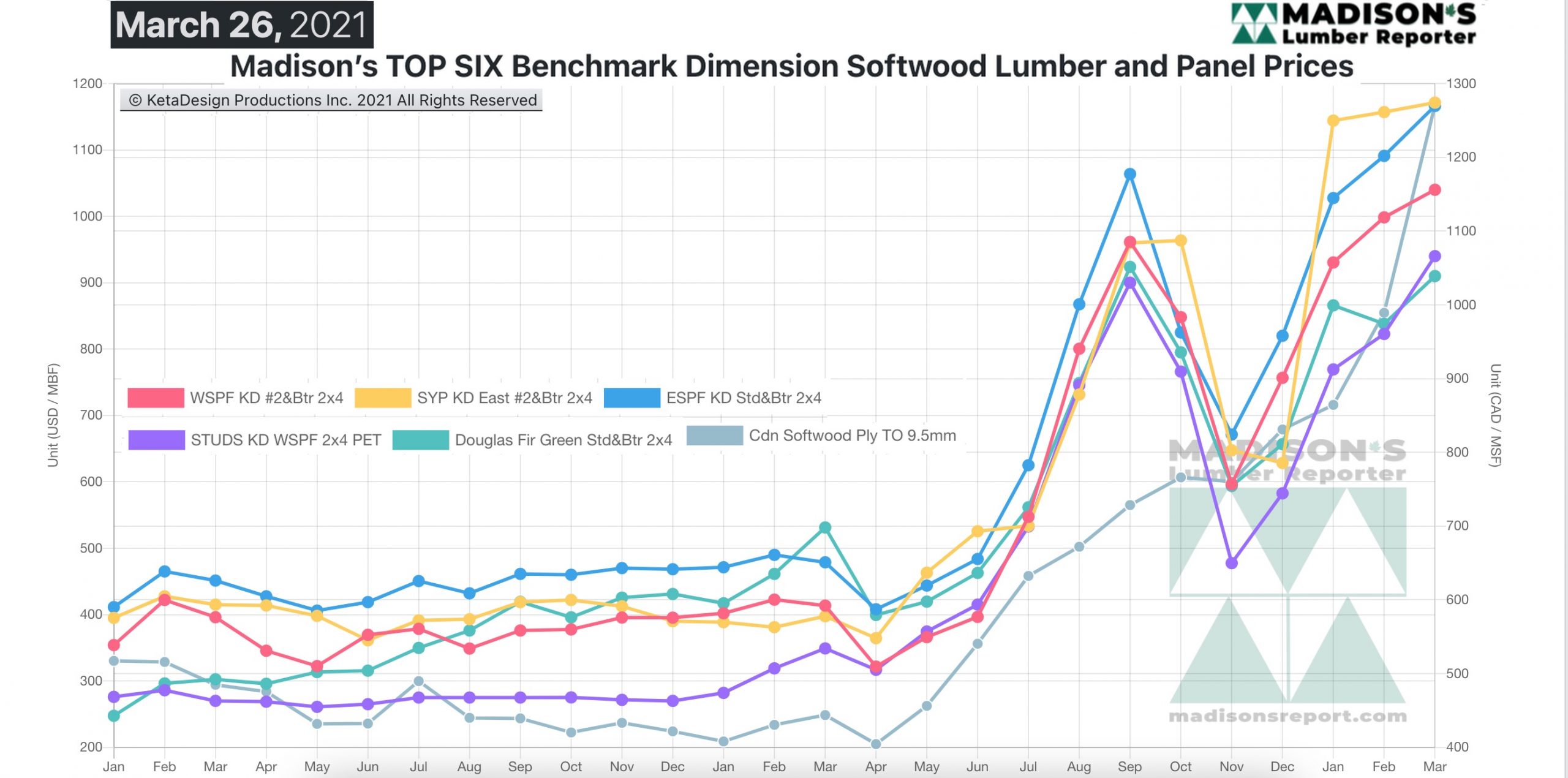

It was an uneven lumber market for the week ending March 26 as print prices came in “all over the place”; some up, some down, and many flat. After waffling for a couple of weeks, the good forward indicator — as mentioned in Madison’s previous few updates — of Canadian Softwood Plywood 9.5 mm Toronto, popped up +$24, or +2%, to end that week at C$1,276 msf, from $1,252 the previous week. The other good forward indicator, Oriented Strand Board 7/16 inches Ontario, soared +$50, or +3.4%, to C$1,475 msf, from $1,425.

There are fewer panel mills than dimension lumber sawmills, so producers are more disciplined in terms of keeping supply close to demand. As well, panel suppliers are better able to withstand counter-offers so those price changes are usually somewhat ahead of dimension lumber price movement.

“Persistently low overall supply ensured that demand remained steady even as buyers sensed prices stabilizing.” — Madison’s Lumber Reporter

Advertisement

For the week ending March 26, U.S. Western S-P-F sawmills stayed the course, pushing their order files into the week of April 19. Buyers were definitely more cautious but their low field inventories and the perpetually undersupplied market forced them back to the table frequently for small volume deals. Players noted an increase in the availability of low-grade WSPF commodities from mills, but if they blinked that supply was gone.

After a fortnight or so of quieter activity, Western S-P-F producers in Canada got busy again. Starting on Tuesday of that week, buyers began to clamour more urgently for new orders as well as those already in the logistical pipeline. Sawmill order files stretched into mid-April on most items, with shipment-lag putting delivery closer to the end of May.

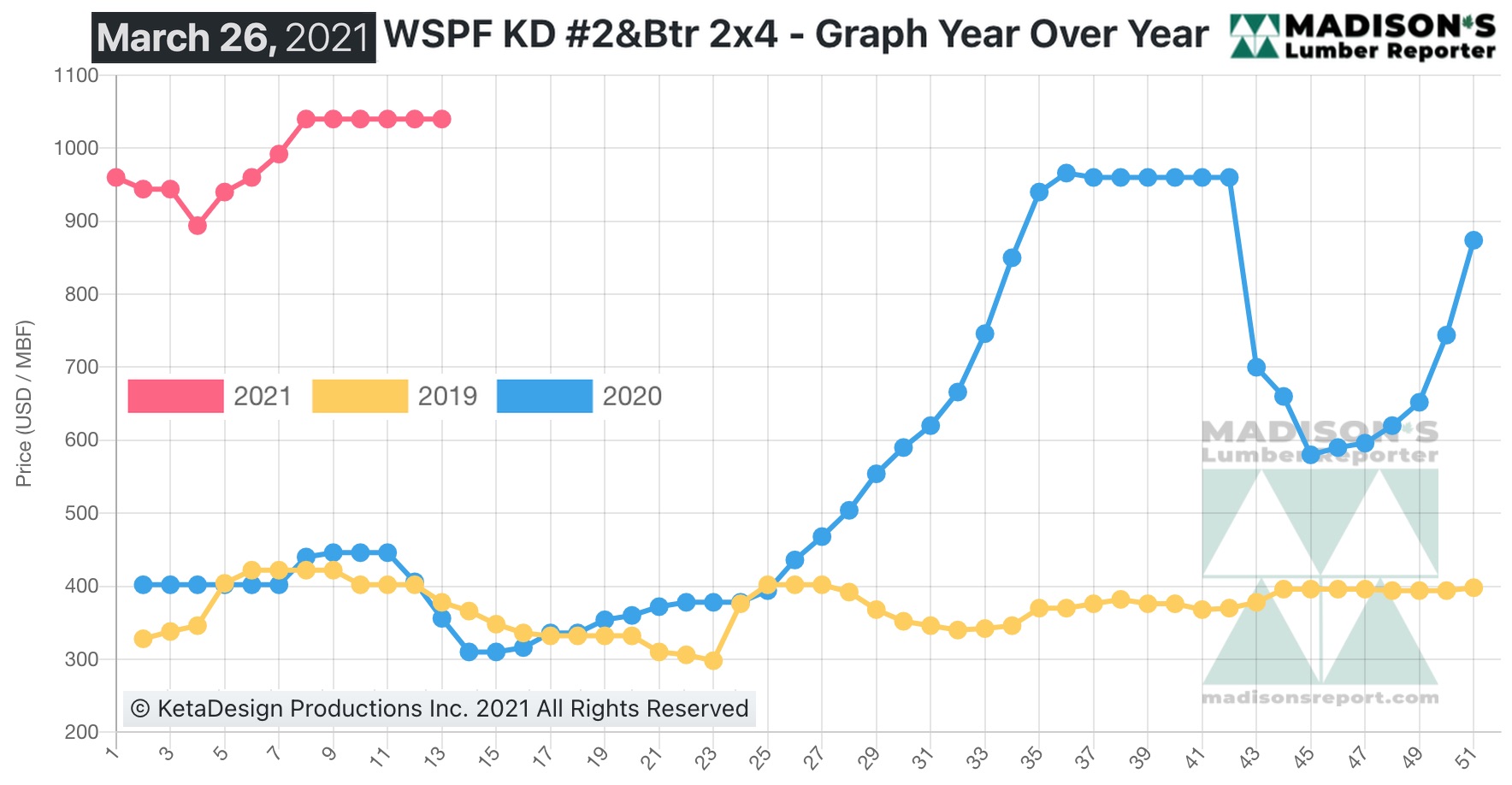

Again staying flat from the previous week, in the week ending Mar. 26, 2021, the price of benchmark softwood lumber commodity item Western S-P-F KD 2×4 #2&Btr remained level at US$1,040 mfbm. That week’s price is again +$42, or +4%, more than one month ago when it was $998.

“Demand for Kiln-Dried Douglas-fir strengthened. Robust sales continued to outstrip comparatively meagre supply as buyers hoped for a break in pricing. Sawmill order files ranged from April 5 to April 19.” — Madison’s Lumber Reporter

Compared to the price one-year-ago, of US$356 mfbm, for the week ending March 26 benchmark softwood lumber item Western S-P-F KD 2×4 #2&Btr was again selling for US$1,040 mfbm which is +684, or +192% more.

Print this page